Financial Fair Play 2.0: The UEFA Club Licensing and Financial Sustainability Regulations

Introduction

On 1 June 2022, the much anticipated UEFA Club Licensing and Financial Sustainability Regulations (the “FSR”) came into full effect, replacing the UEFA Club Licensing and Financial Fair Play Regulations (the “FFP Regulations”).

As part of its swathe of reforms, the FSR have updated UEFA’s club monitoring requirements, with which all clubs competing in UEFA club competitions (i.e., the UEFA Champions League, the UEFA Europa League and the UEFA Conference League (the “Relevant Competitions”)), must comply.

The club monitoring requirements are centred around three pillars: solvency, stability, and cost control. This article examines the key rule changes associated with each pillar.

Solvency

In an attempt to promote the protection of creditors, and to encourage improved solvency amongst clubs, the FSR have amended the pre-existing rules on overdue payables. Relevant payables for these purposes concern only those due to other clubs (such as transfer fees), employees (such as salaries, appearance fees and bonuses), social/tax authorities and (now) UEFA. Payables are considered to be overdue “if they are not paid according to the contractual or legal terms”.

Under the FFP Regulations, clubs were required to settle such payables biannually, on 30 June and 30 September each license season. They also had to provide evidence to UEFA of the same. The new rules provide for an additional deadline (31 December), such that clubs must now settle, and prove that they have settled, overdue payables three times per license season. The FSR also allow clubs an extra fifteen days to meet their obligations in respect of overdue payables. Therefore, payables due by 30 June, 30 September and 31 December during each license season must now be settled by 15 July, 15 October and 15 January respectively. In addition, as noted above, UEFA has been added to the list of persons to whom clubs must have discharged their obligations regarding overdue payables.

UEFA has made clear that it intends to impose tougher financial and sporting sanctions on clubs which fail to comply with the overdue payables rule. As such, the FSR includes a new Article 96.02 which provides that UEFA will consider it an aggravated breach of the FSR if payables are overdue for more than 90 days, which may result in clubs being excluded from future competitions.

The power to exclude clubs from competitions is not new. However the FFP Regulations previously made no reference to it in the context of overdue payables. It will therefore be interesting to see how the UEFA Club Financial Control Body (the “CFCB”), the entity responsible for sanctioning under the FSR, interprets this amendment to the regulations given that it has been relatively reluctant to ban clubs for similar types of breaches in the past.

Stability

At the heart of the stability requirements is the new football earnings rule (the “Football Earnings Rule”), which replaces the break-even rule (the “Break-Even Rule”). The Football Earnings Rule applies to “all clubs admitted to the Relevant Competitions except those clubs that have employee benefit expenses in respect of all employees below EUR 5 million in each of the reporting periods ending in the two calendar years before commencement of the UEFA club competitions.”

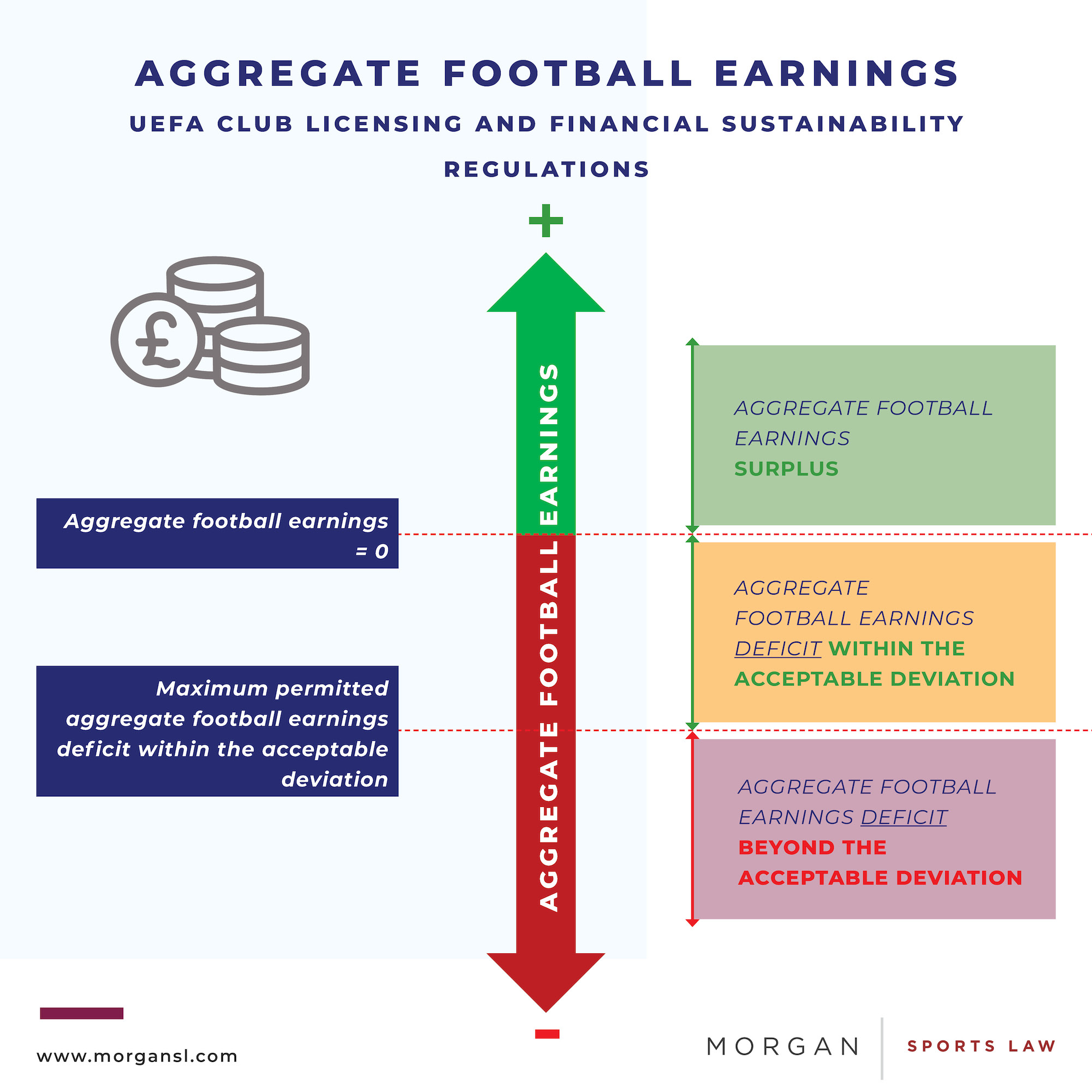

A club will comply with the Football Earnings Rule if it has either an aggregate football earnings surplus or an aggregate football earnings deficit within the acceptable deviation. Football earnings are calculated as the difference between a club’s relevant income and its relevant expenses, and are measured each financial year, referred to within the FSR as a reporting period (“Reporting Period”). A club’s aggregate football earnings, and therefore its compliance with the Football Earnings Rule, are measured over three successive Reporting Periods, collectively referred to within the FSR as a monitoring period (“Monitoring Period”). Thus, a club’s aggregate football earnings are the sum of its football earnings over a Monitoring Period, which includes the Reporting Period ending in the calendar year in which the Relevant Competitions commence (which is referred to as Reporting Period T within the FSR).

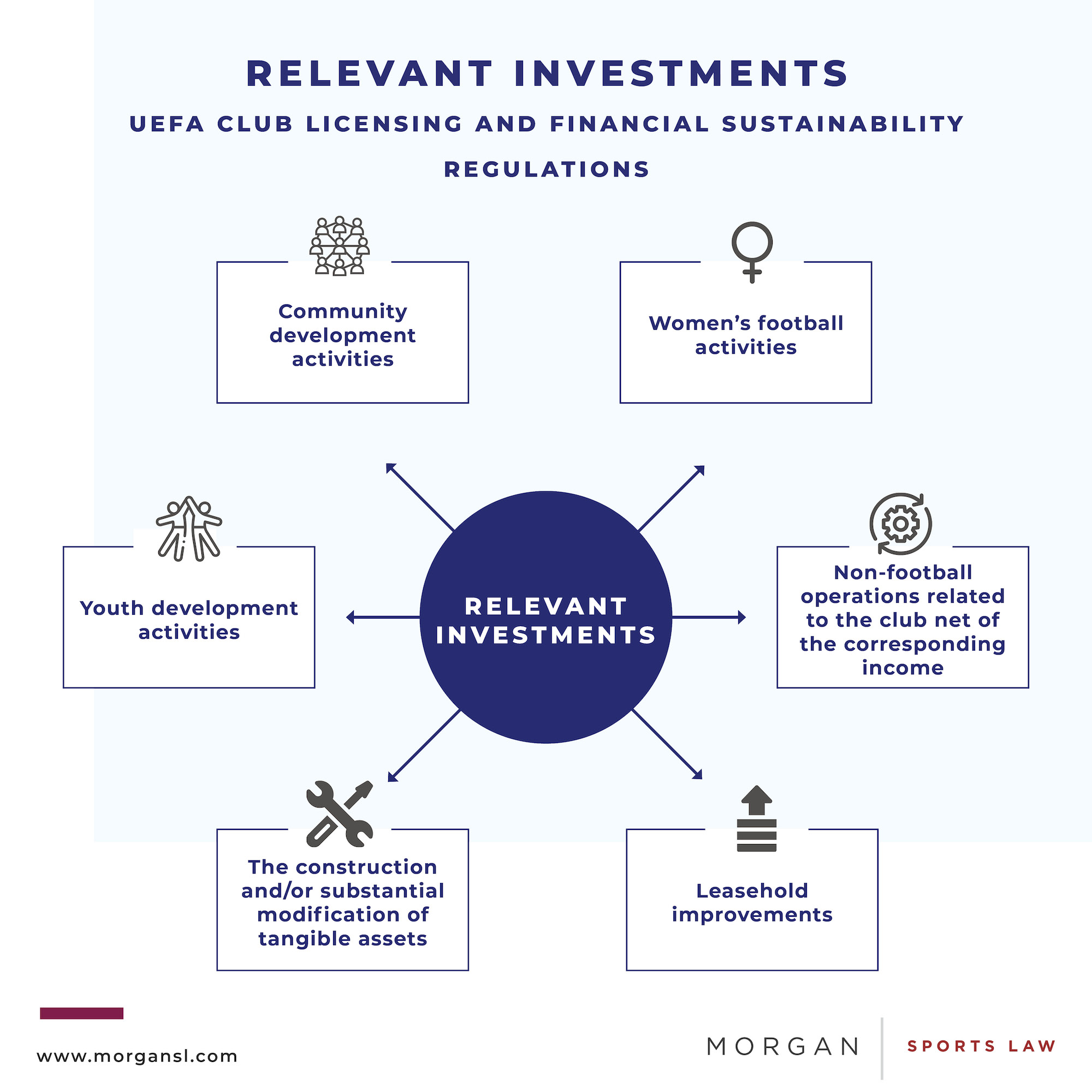

Aggregate football earnings can be adjusted upwards where clubs make relevant investments. Relevant investments, for the purposes of the FSR, are investments in those activities which provide long-term benefits for football, such as expenditure directly attributable to youth development activities or women’s football.

If a club’s aggregate football earnings are positive, then it has an aggregate football earnings surplus and will be deemed to have complied with the Football Earnings Rule.

If a club’s aggregate football earnings are negative, then it has an aggregate football earnings deficit and it is necessary to determine whether that deficit falls within the acceptable deviation.

The acceptable deviation is the maximum possible aggregate football earnings deficit which a club can incur and still be deemed to have complied with the football earning rule. Under the FSR the acceptable deviation is EUR 5 million. However, the deficit can exceed this level, up to a maximum of EUR 60 million, so long as such excess is entirely covered by either contributions (e.g. cash donations) in Reporting Period T or equity at the end of Reporting Period T.

This is one area in which the FSR are less stringent than the old rules, as the maximum permissible excess under the Break-Even Rule in the FFP Regulations was EUR 30 million. However, this seeming relaxation of the rules is largely offset by the FSR’s amendments regarding permitted methods of covering the excess. Under the FFP Regulations, clubs were previously able to cover their excess via contributions or equity during any of the Reporting Periods within the Monitoring Period. As noted above, they can now only do so during Reporting Period T. It is hoped that this change will help to promote better long term financial health amongst clubs.

The acceptable deviation can be further increased by up to EUR 10 million for each Reporting Period within the Monitoring Period in which the club:

- has not been subject to disciplinary measures in respect of the club monitoring requirements;

- is not subject to a settlement agreement with the CFCB; and

- complies with the financial conditions set out in Annex J: (i) positive equity; (ii) quick ratio; (iii) sustainable debt; and (iv) going concern.

This an entirely new concept introduced by the FSR. It has partly been implemented as a response to the Covid-19 pandemic so as not to penalise clubs which are generally financially stable but suffer an unexpected reduction in football related income.

The sanctions which the CFCB can choose to impose for breaches of the Football Earnings Rule are identical to the sanctions that were available in respect of breaches of the Break-Even Rule. As such, the CFCB can take any of the disciplinary measures listed in Article 29 of the Procedural Rules Governing the UEFA Club Financial Control Body 2021 (the “CFCB Procedural Rules”) against clubs and/or individuals whom violate the stability requirements.

To give clubs an opportunity to adapt to the above described changes, the Break-Even Rule will continue to apply for the 2022/23 season. From then on, the Football Earnings Rule will be implemented gradually and will only be in full effect come the 2025/26 season.

Cost Control

The cost control requirements have been newly introduced by the FSR and have no predecessor within the FFP Regulations. They apply to all clubs which qualify for the group stages of the Relevant Competitions, except those that have employee benefit expenses in respect of all employees below EUR 30 million in Reporting Period T and the Reporting Period immediately prior to that.

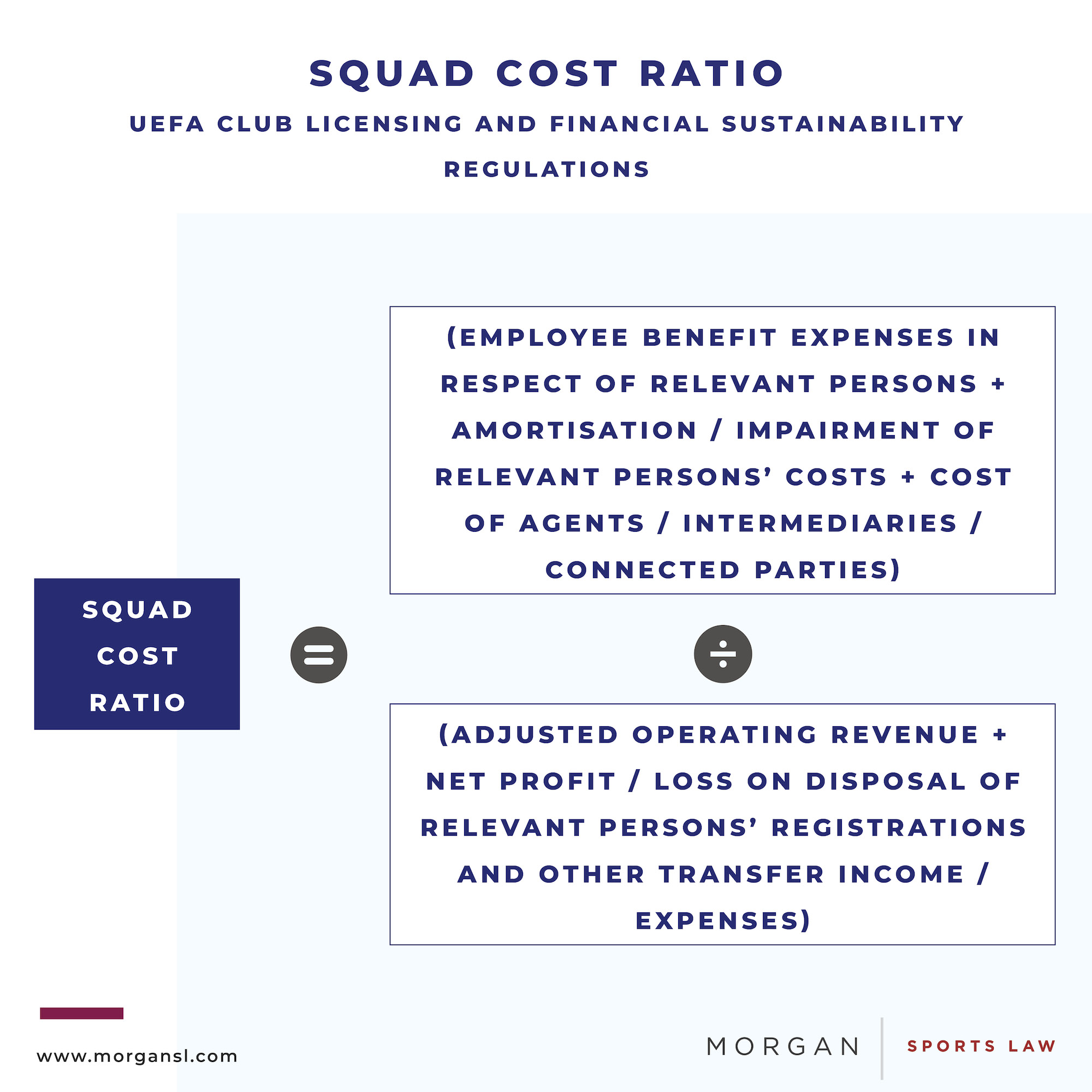

The primary focus of the cost control requirements is the squad cost rule, which provides that a club’s “squad cost ratio” must be no greater than 70% per season.

A club’s squad cost ratio is calculated as the sum of:

- employee benefit expenses in respect of relevant persons;

- amortisation/impairment of relevant persons’ costs; and

- cost of agents/intermediaries/connected parties,

divided by the sum of:

- adjusted operating revenue; and

- net profit/loss on disposal of relevant persons’ registrations and other transfer income/expenses.

Thus, the new rule essentially limits a club’s expenditure on wages for players and coaches, transfer fees and agents’ fees to 70% of its total annual revenue.

A club in breach of the cost control requirements will be subject to financial disciplinary measures imposed by the CFCB. Where a club is considered to have committed a “significant breach” of the squad cost rule, the CFCB will apply “additional disciplinary measures” on top of any financial penalty imposed. Such “additional disciplinary measures” can include a prohibition on registering new players in the Relevant Competitions and disqualification and/or exclusion from the Relevant Competitions.

To allow clubs to adapt to the changes, UEFA have decided that the squad cost rule will be implemented gradually. Accordingly, no cost control requirements will be applied for the 2022/23 season. Then, in the 2023/24 season, the squad cost ratio will be set at 90%, this will fall to 80% for 2024/25 and then to 70% for 2025/26.

Conclusion

It is apparent from the above that, contrary to the assertions of some commentators, the Financial Fair Play regime is not dead. Rather, the FSR have merely updated the FFP Regulations in an attempt to make them more suitable to govern the modern game. UEFA’s stated rational for implementing the new rules is to encourage greater financial sustainability amongst clubs, taking into account the challenges of the post-Covid-19 world and the greater globalisation and technological innovation which has occurred in European football since 2010. How effective the FSR will be in achieving its aims remains to be seen.

Authored By

Ben Cisneros

Trainee Solicitor

Sam Kasoulis

Paralegal

Morgan Sports Law has experience in acting for clubs before UEFA’s disciplinary bodies and the Court of Arbitration for Sport. Please contact William Sternheimer (Partner - Football Disputes) with any enquiries.

Footnote

1. FSR, Article 79.01. There are carve-outs which exempt some clubs from certain provisions. This article sets out those carve-outs where applicable.

2. FSR, Article 79.02

3. FSR, Annex H.1.1

4. FFP Regulations, Articles 65-66bis

5. FSR, Articles 80-83

6. Ibid.

7. FSR, Article 83

8. FSR, Article 79.04

9. FSR, Article 90. Relevant income and relevant expenses are respectively defined at Annex J.2 and J.3 of the FSR. Pursuant to Article 84.03 of the FSR, relevant income and relevant expenses must be adjusted to ensure that they reflect fair value. Fair value is defined at Annex J.7 of the FSR. Previously, only related party transactions had to be fair value, whereas now all transactions must be fair value.

10. FSR, Article 86.01

11. FSR, Article 85

12. FSR, Article 86.03

13. FSR, Article 89

14. FSR, Articles 86.04 and 90.01.a

15. FSR, Article 86.04 and 90.01.b

16. FSR, Article 87.01

17. FSR, Article 87.02. The term "contributions" is defined at Article 88 of the FSR. These include, for example, "monies received from any party as a donation (e.g. an unconditional gift) or a waiver of liability ". In this context, "equity" refers to a club’s assets less its liabilities, as set out in its annual financial statements or interim financial statements as applicable (see FSR, Article 69).

18. FFP Regulations, Article 61.2

19. FFP Regulations, Article 61.3.a

20. A club has positive equity if its assets exceed its liabilities (see FSR, Article 69.02).

21. Clubs are required to report a quick ratio equal to or above 1 at the end of each Reporting Period. The quick ratio is calculated as total current assets less inventories divided by total current liabilities (see FSR, Annex J.6.1.b).

22. FSR, Article 87.03

23. FSR, Article 104.01

24. FSR, Article 79.05

25. FSR, Article 93

26. FSR, Article 92

27. FSR, Article 96.04 and Annex L

28. As defined in FSR, Annex L.2

29. FSR, Article 96.04 and Annex L.1.c

30. See Article 29.1 of the CFCB Procedural Rules

31. FSR, Article 104.02